“`html

The Strangle Options Strategy: A Guide

The strangle is an options trading strategy that involves simultaneously buying both an out-of-the-money (OTM) call option and an out-of-the-money put option on the same underlying asset, with the same expiration date. The “out-of-the-money” aspect is crucial; the call’s strike price is above the current market price, and the put’s strike price is below.

Why use a Strangle?

Strangles are typically employed when a trader believes the underlying asset’s price will experience a significant move, but is unsure of the direction. It’s a volatility play, profiting from large price swings regardless of whether the price goes up or down. They are particularly attractive when volatility is low and expected to increase. Earnings announcements, significant news events, or periods of market uncertainty are common scenarios where strangles might be implemented.

How it Works:

The trader pays a premium for both the call and put options. The combined premium represents the maximum potential loss. To profit, the price of the underlying asset must move significantly enough in either direction to offset the cost of both options.

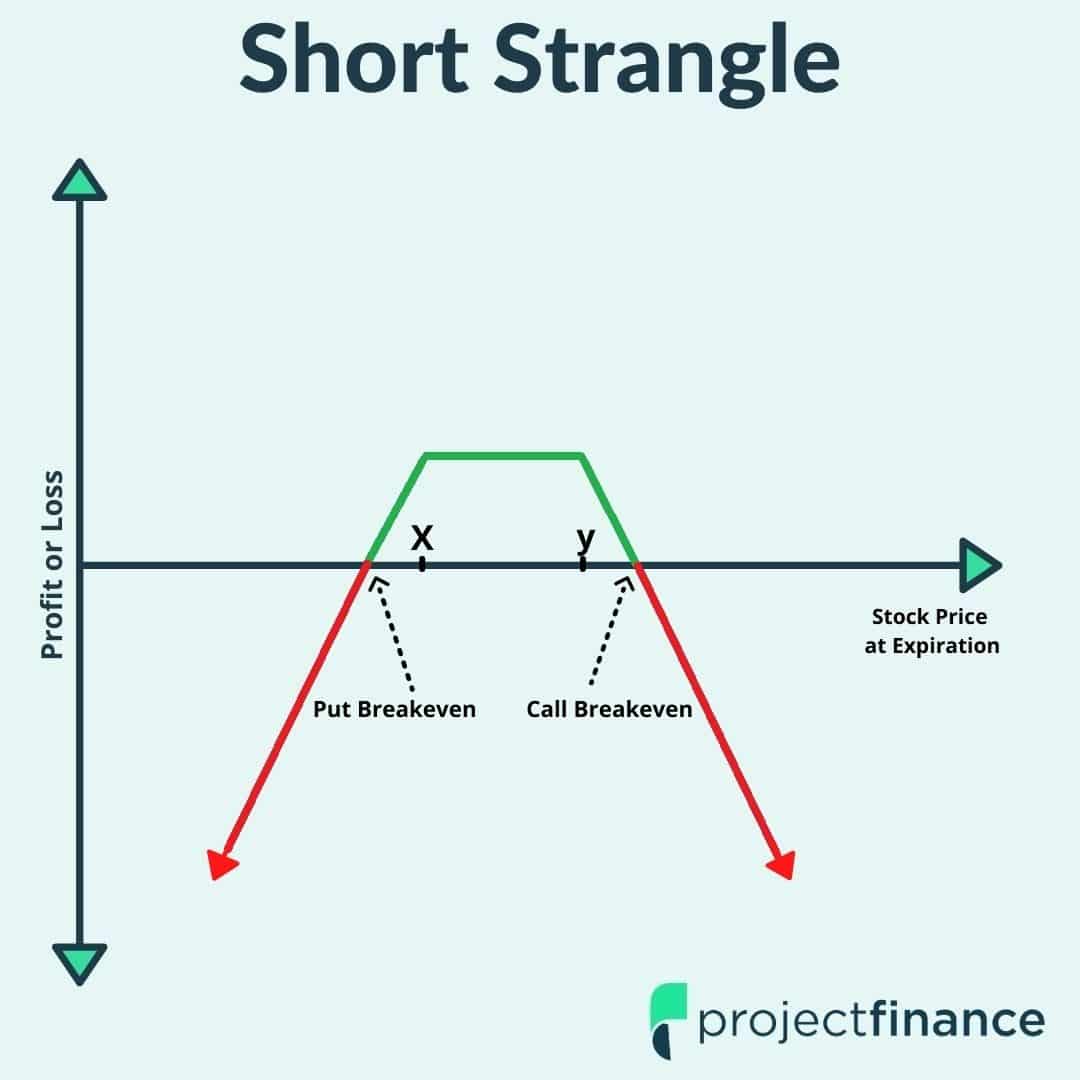

Profit and Loss Profile:

- Maximum Loss: Limited to the total premium paid for both options. This occurs if the asset’s price at expiration remains between the strike prices of the put and the call.

- Maximum Profit: Theoretically unlimited on the upside (if the asset price rises significantly) and limited to the strike price of the put minus the premium paid on the downside (if the asset price falls to zero).

- Break-Even Points: There are two break-even points. The upper break-even is the call’s strike price plus the total premium paid. The lower break-even is the put’s strike price minus the total premium paid.

Advantages:

- Potential for significant profit if the underlying asset moves substantially.

- Defined risk (the maximum loss is limited to the premium paid).

- Can profit from either upward or downward price movements.

Disadvantages:

- Requires a significant price movement to become profitable.

- Time decay (theta) can erode the value of the options, especially as expiration approaches.

- Can be expensive to implement, as you are paying for two options contracts.

Considerations:

Choosing appropriate strike prices is crucial. Wider strike prices require a larger price movement to become profitable but reduce the initial cost. Narrower strike prices are cheaper but require a more precise prediction of price direction. Time to expiration also plays a role. Longer-dated options are more expensive but provide more time for the price to move. Carefully manage risk and consider implied volatility when implementing this strategy. It’s generally not suitable for novice traders.

“`

400×229 strangle finance explained from tiblio.com

400×229 strangle finance explained from tiblio.com  807×583 covered strangle option strategy works guide visuals from www.projectfinance.com

807×583 covered strangle option strategy works guide visuals from www.projectfinance.com  600×407 strangle option strategy beginners guide stock market from boomingbulls.com

600×407 strangle option strategy beginners guide stock market from boomingbulls.com  1080×1080 short strangle explained ultimate visual guide projectfinance from www.projectfinance.com

1080×1080 short strangle explained ultimate visual guide projectfinance from www.projectfinance.com  960×653 strangle options strategy long short strangle redot blog from redot.com

960×653 strangle options strategy long short strangle redot blog from redot.com  2560×1704 short strangle trading strategy adjustments booming bulls academy from boomingbulls.com

2560×1704 short strangle trading strategy adjustments booming bulls academy from boomingbulls.com  547×297 short strangle sell strangle option strategy explained from www.chittorgarh.com

547×297 short strangle sell strangle option strategy explained from www.chittorgarh.com  1080×1080 options straddle strangle differ projectfinance from www.projectfinance.com

1080×1080 options straddle strangle differ projectfinance from www.projectfinance.com  1560×1070 straddle strangle options strategy option alpha from optionalpha.com

1560×1070 straddle strangle options strategy option alpha from optionalpha.com  750×532 short strangle option strategy complete guide geekrar from www.geekrar.com

750×532 short strangle option strategy complete guide geekrar from www.geekrar.com  479×289 short strangle options strategy risks benefits strategy from www.adigitalblogger.com

479×289 short strangle options strategy risks benefits strategy from www.adigitalblogger.com  1400×706 strangle option strategy definition types benefits from www.stockgro.club

1400×706 strangle option strategy definition types benefits from www.stockgro.club  574×368 strangle strategy options trading roz paisa banao from www.rozpaisabanao.com

574×368 strangle strategy options trading roz paisa banao from www.rozpaisabanao.com  889×758 option strangle strategy strangle options from www.warsoption.com

889×758 option strangle strategy strangle options from www.warsoption.com  932×550 strangle tradingview india from in.tradingview.com

932×550 strangle tradingview india from in.tradingview.com  531×640 strangle options trading innovative income strategy heroturkonet from www.heroturko.net

531×640 strangle options trading innovative income strategy heroturkonet from www.heroturko.net  2560×1097 straddle strangle options strategy from insights.masterworks.com

2560×1097 straddle strangle options strategy from insights.masterworks.com  750×471 strangle options strategy helpful guide traders from www.moomoo.com

750×471 strangle options strategy helpful guide traders from www.moomoo.com  1500×844 strangle option strategy works dhan blog from blog.dhan.co

1500×844 strangle option strategy works dhan blog from blog.dhan.co :max_bytes(150000):strip_icc()/dotdash_INV_final_Get_A_Strong_Hold_On_Profit_With_Strangles_Jan_2021-01-a99fea66493449eea01e450feb7475e2.jpg) 2271×1480 strong hold profit strangles from www.investopedia.com

2271×1480 strong hold profit strangles from www.investopedia.com :max_bytes(150000):strip_icc()/dotdash_INV_final_Get_A_Strong_Hold_On_Profit_With_Strangles_Jan_2021-03-d40b125474754c73aec56a75b19032e9.jpg) 1500×1075 strangle strategy hold profits from www.investopedia.com

1500×1075 strangle strategy hold profits from www.investopedia.com  1024×1024 strangle strategy harnessing wide price swings options from moneymunch.com

1024×1024 strangle strategy harnessing wide price swings options from moneymunch.com  1024×743 strangle strategy forex trading walletinvestor magazin from walletinvestor.com

1024×743 strangle strategy forex trading walletinvestor magazin from walletinvestor.com  400×322 strangle options trading innovative income strategy saad tariq from gripforex.com

400×322 strangle options trading innovative income strategy saad tariq from gripforex.com  750×375 strangle strategy trade options trading asia from www.gotradingasia.com

750×375 strangle strategy trade options trading asia from www.gotradingasia.com  473×471 strangle trading strategy created from jairo-kkennedy.blogspot.com

473×471 strangle trading strategy created from jairo-kkennedy.blogspot.com  490×281 master options trading long strangle from masteroptionstrading.blogspot.com

490×281 master options trading long strangle from masteroptionstrading.blogspot.com  2000×1333 strangle option definition investing dictionary news from money.usnews.com

2000×1333 strangle option definition investing dictionary news from money.usnews.com  1002×494 strangle option strategy meaning longshort graph from www.wallstreetmojo.com

1002×494 strangle option strategy meaning longshort graph from www.wallstreetmojo.com  660×210 strangle learn options trading from marketchameleon.com

660×210 strangle learn options trading from marketchameleon.com  998×521 understanding strangle options strategy currency options from www.publish0x.com

998×521 understanding strangle options strategy currency options from www.publish0x.com  825×597 long strangle option strategy warsoption from www.warsoption.com

825×597 long strangle option strategy warsoption from www.warsoption.com  735×1103 option strangle from www.options-trading-mastery.com

735×1103 option strangle from www.options-trading-mastery.com