Finance mix, also referred to as capital structure, represents the specific blend of debt and equity a company uses to finance its operations and growth. It’s a critical decision that significantly impacts a company’s profitability, risk, and ultimately, its value. Finding the optimal finance mix is about balancing the advantages and disadvantages of each component to create a structure that minimizes the cost of capital while aligning with the company’s strategic goals and risk appetite.

Debt financing involves borrowing money that must be repaid with interest. Its primary advantage is the tax deductibility of interest payments, which effectively lowers the cost of borrowing. Debt can also enhance returns to equity holders in profitable periods, a concept known as financial leverage. However, excessive debt increases financial risk, as the company is obligated to make fixed interest and principal payments regardless of its earnings. High debt levels can lead to financial distress if the company faces economic downturns or internal challenges. Furthermore, too much debt can limit a company’s future borrowing capacity, hindering its ability to seize opportunities or respond to unforeseen circumstances.

Equity financing, on the other hand, represents ownership in the company. It doesn’t require fixed payments like debt, providing greater financial flexibility, especially during periods of low profitability. Equity also strengthens a company’s balance sheet, making it appear less risky to creditors and investors. However, equity dilutes existing ownership, distributing profits across a larger shareholder base. Moreover, equity doesn’t offer the tax advantages that debt does. The cost of equity, often estimated using models like the Capital Asset Pricing Model (CAPM), can be higher than the after-tax cost of debt, particularly for mature companies with established track records.

Determining the optimal capital structure is a complex process influenced by several factors. These include the company’s industry, size, stage of development, profitability, growth prospects, and management’s risk tolerance. Companies in stable industries with predictable cash flows can typically handle more debt than those in volatile or emerging sectors. Smaller, younger companies may rely more on equity initially due to limited access to debt markets and a shorter credit history. Highly profitable companies might leverage debt to boost returns on equity, while those with limited profitability might prioritize equity to reduce financial risk.

Several theoretical frameworks provide guidance on capital structure decisions. The Modigliani-Miller (MM) theorem, in its simplest form, suggests that a company’s value is independent of its capital structure in a perfect market. However, real-world imperfections like taxes, bankruptcy costs, and information asymmetry significantly influence capital structure choices. The trade-off theory balances the tax benefits of debt against the costs of financial distress. The pecking order theory suggests companies prefer internal financing (retained earnings) followed by debt, and finally equity, as a last resort, to minimize adverse selection problems. Market timing theory suggests companies issue equity when valuations are high and debt when valuations are low. In practice, a company’s actual capital structure is often a pragmatic mix of these theoretical considerations, adapted to its specific circumstances and market conditions. Continuous monitoring and adjustments to the finance mix are crucial for maintaining financial health and maximizing shareholder value in a dynamic business environment.

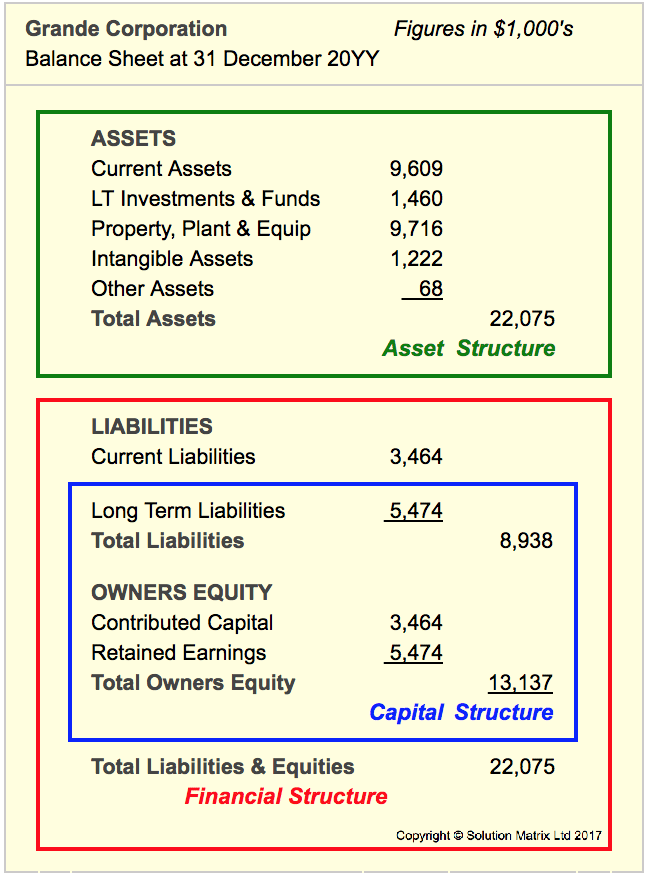

650×881 financial structure capital structure capitalization leverage from www.business-case-analysis.com

650×881 financial structure capital structure capitalization leverage from www.business-case-analysis.com  989×715 capital structure decisions importance factors tips from efinancemanagement.com

989×715 capital structure decisions importance factors tips from efinancemanagement.com  1024×600 capital structure from corporatefinanceinstitute.com

1024×600 capital structure from corporatefinanceinstitute.com  480×300 determining financial mix capital structure prezi from prezi.com

480×300 determining financial mix capital structure prezi from prezi.com  322×156 capital structure makeup management guru management guru from www.managementguru.net

322×156 capital structure makeup management guru management guru from www.managementguru.net  720×540 capital structure optimal financial mix powerpoint from www.slideserve.com

720×540 capital structure optimal financial mix powerpoint from www.slideserve.com  1024×640 capital structure financial structure difference from differencebtw.com

1024×640 capital structure financial structure difference from differencebtw.com  1024×768 capital structure powerpoint id from www.slideserve.com

1024×768 capital structure powerpoint id from www.slideserve.com  1280×720 identify capital structure firm firm alter financial mix from www.slidegeeks.com

1280×720 identify capital structure firm firm alter financial mix from www.slidegeeks.com  720×540 finding financing mix capital structure decision from www.slideserve.com

720×540 finding financing mix capital structure decision from www.slideserve.com  1280×720 role corporate finance capital structure decisions corporate from www.slideteam.net

1280×720 role corporate finance capital structure decisions corporate from www.slideteam.net  960×720 firm alter financial mix rethinking capital structure decision from www.slideteam.net

960×720 firm alter financial mix rethinking capital structure decision from www.slideteam.net  960×720 firm alter financial mix understanding capital structure from www.slideteam.net

960×720 firm alter financial mix understanding capital structure from www.slideteam.net  180×234 understanding capital structure balancing debt equity from www.coursehero.com

180×234 understanding capital structure balancing debt equity from www.coursehero.com  330×186 multiple ratios defining capital structure capital structure from www.slideteam.net

330×186 multiple ratios defining capital structure capital structure from www.slideteam.net  678×241 financing capital structure from www.brainkart.com

678×241 financing capital structure from www.brainkart.com  650×302 financial markets corporate decision making dissertation from study-aids.co.uk

650×302 financial markets corporate decision making dissertation from study-aids.co.uk  1200×675 corporate finance fundamentals optimal capital structure dorothy from medium.com

1200×675 corporate finance fundamentals optimal capital structure dorothy from medium.com  1024×768 corporate finance lecture introduction capital structure from www.slideserve.com

1024×768 corporate finance lecture introduction capital structure from www.slideserve.com  602×504 capital structure financial management class notes commerce from commerceaspirant.com

602×504 capital structure financial management class notes commerce from commerceaspirant.com  180×233 understanding optimal capital structure corporate finance hero from www.coursehero.com

180×233 understanding optimal capital structure corporate finance hero from www.coursehero.com  1024×768 capital structure finance firm powerpoint from www.slideserve.com

1024×768 capital structure finance firm powerpoint from www.slideserve.com  240×320 corporate finance capital structure financing decisions from pdf4pro.com

240×320 corporate finance capital structure financing decisions from pdf4pro.com  588×343 financing decisions capital structure ca inter fm notes gst guntur from gstguntur.com

588×343 financing decisions capital structure ca inter fm notes gst guntur from gstguntur.com