“`html

Calculating Net Present Value (NPV)

Net Present Value (NPV) is a crucial financial metric used in capital budgeting and investment planning. It helps determine whether a project or investment is likely to be profitable by comparing the present value of future cash inflows to the initial investment, also considering the time value of money.

The core concept behind NPV is that money received today is worth more than the same amount received in the future. This is due to factors like inflation and the potential to earn interest or returns on investments. NPV accounts for this by discounting future cash flows back to their present value using a discount rate, which represents the required rate of return or the opportunity cost of capital.

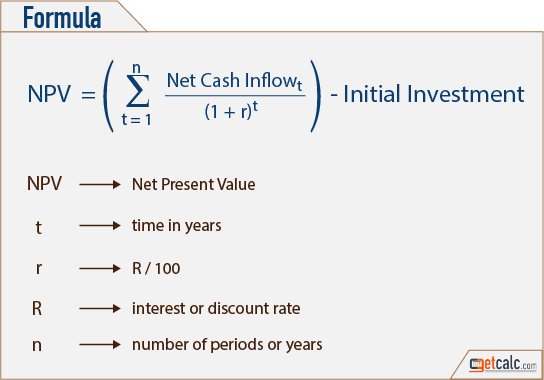

The NPV Formula

The formula for calculating NPV is as follows:

NPV = Σ [CFt / (1 + r)t] – Initial Investment

Where:

- CFt = Cash flow in period t

- r = Discount rate (required rate of return)

- t = Time period (e.g., year)

- Σ = Summation (summing the present values of all cash flows)

Steps to Calculate NPV

- Estimate Cash Flows: Project all future cash inflows and outflows associated with the investment. This includes the initial investment (usually a negative value) and all subsequent revenues and expenses.

- Determine the Discount Rate: Select an appropriate discount rate that reflects the risk and opportunity cost of the investment. This rate often represents the company’s weighted average cost of capital (WACC) or the required rate of return demanded by investors.

- Calculate Present Value of Each Cash Flow: Discount each future cash flow back to its present value using the discount rate and the corresponding time period. This involves dividing each cash flow by (1 + r) raised to the power of t.

- Sum the Present Values: Add up all the present values of the cash flows, including the initial investment (which is already in present value terms).

- Interpret the Result:

- Positive NPV: Indicates that the investment is expected to be profitable and generate more value than it costs. It is generally considered a good investment.

- Negative NPV: Suggests that the investment is expected to result in a loss. It is generally not recommended.

- Zero NPV: Means the investment is expected to break even, neither creating nor destroying value. In this case, other factors may influence the decision.

Example

Suppose a project requires an initial investment of $10,000 and is expected to generate cash flows of $3,000 per year for the next 5 years. The required rate of return (discount rate) is 10%.

Using the NPV formula:

NPV = ($3,000 / (1 + 0.10)1) + ($3,000 / (1 + 0.10)2) + ($3,000 / (1 + 0.10)3) + ($3,000 / (1 + 0.10)4) + ($3,000 / (1 + 0.10)5) – $10,000

NPV ≈ $1,372.35

Since the NPV is positive, the project is expected to be profitable and a worthwhile investment.

Limitations: NPV calculations rely on accurately projecting future cash flows and selecting an appropriate discount rate, both of which can be challenging. Sensitivity analysis, where different discount rates and cash flow scenarios are tested, can help assess the robustness of the NPV result.

“`

544×380 calculate npv haiper vrogueco from www.vrogue.co

544×380 calculate npv haiper vrogueco from www.vrogue.co  1024×1013 npv calculator calculate net present finpins from finlightened.com

1024×1013 npv calculator calculate net present finpins from finlightened.com  473×422 calculate npv excel finance class investment criteria npv from miguellas.blogspot.com

473×422 calculate npv excel finance class investment criteria npv from miguellas.blogspot.com  1391×410 npv calculator propertymetrics from propertymetrics.com

1391×410 npv calculator propertymetrics from propertymetrics.com  1920×625 solved npv calculation calculate npv cheggcom from www.chegg.com

1920×625 solved npv calculation calculate npv cheggcom from www.chegg.com  585×395 npv calculator investing post from investpost.org

585×395 npv calculator investing post from investpost.org  1000×692 calculate npv stock stockoc from stockoc.blogspot.com

1000×692 calculate npv stock stockoc from stockoc.blogspot.com  1260×661 master investment decisions essential net present from www.azibo.com

1260×661 master investment decisions essential net present from www.azibo.com  1024×642 net present npv calculator hsiu hsius blog from blog.hsiuhsiu.com

1024×642 net present npv calculator hsiu hsius blog from blog.hsiuhsiu.com  1550×524 quick valuation net present npv calculator eloquens from www.eloquens.com

1550×524 quick valuation net present npv calculator eloquens from www.eloquens.com  961×625 calculate risk adjusted npv from dangelo-well-conley.blogspot.com

961×625 calculate risk adjusted npv from dangelo-well-conley.blogspot.com  1024×171 calculate net present npv forage from www.theforage.com

1024×171 calculate net present npv forage from www.theforage.com  749×488 npv calculator calculate net present from www.gigacalculator.com

749×488 npv calculator calculate net present from www.gigacalculator.com  770×853 net present npv calculator from ncalculators.com

770×853 net present npv calculator from ncalculators.com  689×758 understand net present npv planning engineer est from planningengineer.net

689×758 understand net present npv planning engineer est from planningengineer.net  1411×501 net present npv calculator project managementinfo from project-management.info

1411×501 net present npv calculator project managementinfo from project-management.info  444×319 npv net present formula meaning calculator from cleartax.in

444×319 npv net present formula meaning calculator from cleartax.in  2046×974 solved calculate npv investment cheggcom from www.chegg.com

2046×974 solved calculate npv investment cheggcom from www.chegg.com :max_bytes(150000):strip_icc()/dotdash_Final_Net_Present_Value_NPV_Jul_2020-01-eea50904f90744e4b1172a9ef38df13f.jpg) 1500×931 net present npv means steps calculate from investguiding.com

1500×931 net present npv means steps calculate from investguiding.com :max_bytes(150000):strip_icc()/ScreenShot2019-06-20at10.46.59AM-f30499c2303c44a5a883c6c1e676569b.png) 1296×730 net present npv from www.investopedia.com

1296×730 net present npv from www.investopedia.com  650×429 npv net present calculation table from www.researchgate.net

650×429 npv net present calculation table from www.researchgate.net  666×430 npv formula excel blog risovanii urokax fotosopa from www.pscraft.ru

666×430 npv formula excel blog risovanii urokax fotosopa from www.pscraft.ru